The impact of deeper PPI use at Fusion Microfinance >

An interview with Devesh Sachdev, Founder & CEO and Shalini Singh, Senior Manager – Social Performance at Fusion Microfinance

Fusion Microfinance (Fusion) is a registered Non-Banking Financial Company – Microfinance Institution (NBFC – MFI) set up in 2010 in India. It operates through the Joint Liability Group lending model pioneered by the Grameen Bank and targets underprivileged women clients living in rural and semi-urban areas. It focuses on reaching out to the unbanked and provides financial services to women entrepreneurs belonging to the economically and socially deprived sections of society. Fusion does not restrict itself to providing credit support alone but also provides financial education to its clients to enable them to manage finances in their personal and professional lives. Fusion aspires to create value and balanced growth for all its stakeholders while keeping clients at the center of its efforts. Currently, Fusion operates in 18 states across India and has reached more than 0.12 million clients as of September 2018.

1. When did your organization start using the PPI, and why? What was the need you were hoping to address?

When we started operations, early in 2010, we used very rudimentary indicators to measure the poverty of our client households and assess our loan portfolio. Later, we decided to measure our poverty outreach using a scientific tool and zeroed in on the PPI in 2012. Since then, we have been using the PPI as part of our Social Performance Management (SPM). The PPI has allowed us to collect key household data through a simple survey that is easy to understand and quick to administer and use the data to understand the socio-economic status of our clients.

2. Describe the logistics of collecting and using the PPI at your organization.

PPI data is collected from client households by our relationship officers during the compulsory group training activity that is conducted prior to loan disbursal. Key officials from multiple departments at Fusion – Operations, MIS, Audit, Training and SPM collaborate to collect, store, quality check, analyse and report PPI data. We ensure that each of the departments performs their specified tasks and meet deadlines for timely delivery of PPI reports.

3. Can you please let us know how the PPI has helped your organisation in your SPM reporting?

In the first place, as an organization, it is important for us to understand our poverty outreach. This is because our goal of reaching out to unbanked women through financial services comes directly from the mission and vision of the organization. It is also our business strategy to include women coming from deprived socio-economic backgrounds.

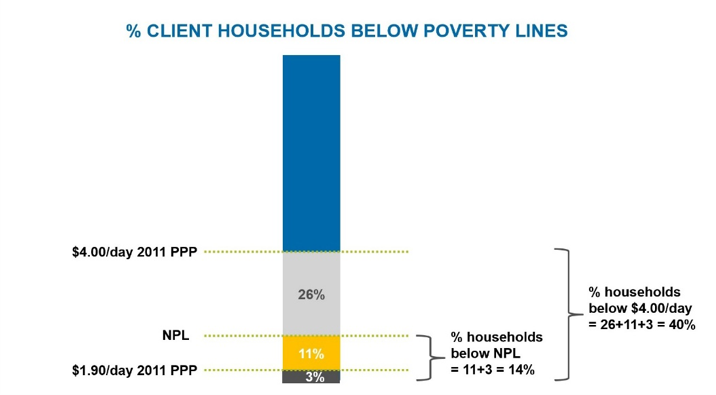

We report the % of our client households below India’s National Poverty Line (NPL), and the World Bank defined International Poverty Line - $1.90/day 2011 PPP. Additionally, we report our outreach below the $4.00/day 2011 PPP Line as well since this poverty line roughly corresponds to the maximum income limit set for borrowers by the Reserve Bank of India (INR 1,00,000 for rural borrowers and INR 1,60,000 for urban borrowers annually).

Poverty rates (% poor client households reached) at an aggregate portfolio level, as measured by the PPI are below:

Additionally, the PPI has allowed us to map poverty status across different client-level indicators such as being from marginalized communities, geography, and occupation. The PPI also makes it possible for us to track changes in the poverty levels of our clients over a period of time.

The tool has provided us with a statistically rigorous yet simple way to continually gauge the proportion of poor client households that we reach, which is why we continue to invest in improving the PPI-related structures and processes at Fusion.

4. Can you let us know about the PSIG1-funded PPI Institutionalisation project? How was Fusion included in the project and what was the technical support you received?

Grameen Foundation India (GFI) communicated their interest in supporting PSIG’s MFI partners on PPI implementation and emphasized the usefulness of the tool to us. During that time, we were planning to transition from India’s 2009 PPI to the new 2011 PPI which had just been released. It was thus an opportune moment for us to join the program. We needed support to understand the updated PPI and seamlessly integrate it across our processes and systems. Additionally, we had two major questions:

(a) If and how we could compare or combine poverty estimates obtained from two different versions of the PPI, and

(b) How we should choose appropriate poverty line(s) for analysis from among the newly-defined poverty lines available in the latest PPI.

Our management team has always been supportive of strengthening our social performance, so we had their approval to participate in this project.

5. How did Fusion ensure smooth implementation of the PPI with support from this project?

As a first step, we secured buy-in from our management team. Proactive participation from other departments ensured that the whole implementation process was smooth. As we progressed, we took initiatives to achieve the outcome specified in each step. At the planning stage for example - different teams i.e. MIS, Audit, training, and operations were appraised about their roles and responsibilities towards adopting the new PPI and integrating it into their operations. The old PPI questionnaire was replaced by the new one in our loan application form. Field staff was trained in administering the new PPI to our clients. Necessary changes were made in our MIS system to facilitate data entry and analysis with the new PPI. Quality audits were conducted once the new PPI was incorporated into our systems, and GFI verified the results of our first audit. Throughout, we made sure to course-correct as needed.

6. What were the benefits of getting support for PPI implementation at Fusion?

Implementation assistance helped us in two ways –

(a) Grameen Foundation India provided advice on additional socio-economic indicators that we could collect along with PPI data during the compulsory group training activity conducted prior to loan disbursal. This included indicators such as occupation, and access to drinking water, sanitation facilities, and other financial services.

(b) We had previously been using India’s 2009 PPI. But as we needed to transition to the new 2011 PPI, we needed support with data analysis and understanding the newly-defined poverty lines in the latest PPI. Through our participation in this project, we received extensive support from GFI on this. At one point in time, we had PPI data from both – the older and newer PPI versions. GFI helped us to compare and combine poverty estimates from both versions. This would have been very difficult for us to do on our own without their support.

[1] The Department for International Development (DFID) leads the UK’s work to end extreme poverty. Through its Poorest States Inclusive Growth (PSIG) program in India, DFID, in collaboration with the Small Industries Development Bank of India (SIDBI) aims to address the uneven gains from India’s economic growth across states. PSIG funded a project to institutionalize use of the Poverty Probability Index® (PPI®) across Microfinance Institutions in 4 states in India – Madhya Pradesh, Orissa, Uttar Pradesh, and Bihar in 2015. This project was implemented by Grameen Foundation India. Fusion participated in this project and received technical support in transitioning to India’s latest PPI – which is based on survey data from 2011. Prior to the project, Fusion was using the previous version of India’s PPI, which was based on survey data from 2009.