India Poverty Outreach Report Provide Insights on the State of Microfinance >

Over the past year and a half, Grameen Foundation India (GFI) conducted a new poverty outreach study of microfinance institution (MFI) clients across Bihar, Madhya Pradesh, Orissa and Uttar Pradesh – four focus states of the Poorest States Inclusive Growth Programme (PSIG). The study evaluates the MFI portfolios against the base population’s poverty profile in these four states and builds understanding of microfinance clients by drawing parallels between poverty data and other socio-economic indicators. The Progress Out of Poverty Index® was used to segment households into five categories:

- ‘Ultra Poor’ – Below National Poverty Line for India

- ‘Very Poor’ – Between National Tendulkar Line and $1.25/day (2005 PPP)

- ‘Poor’ – Between $1.25/day and $1.88/day (2005 PPP)

- ‘Borderline Poor’ – Between $1.88/day and $2.50/day (2005 PPP)

- Above $2.50/day

PSIG- a SIDBI and DFID UK driven program is being executed in Bihar, Madhya Pradesh, Odisha and Uttar Pradesh and was also the focus of the study. One of the program’s objectives is to expand microfinance services across the above mentioned four states which are among the poorest in India. This includes building and expanding community-based and microfinance institutions, promoting the delivery of a cost-effective, diverse array of financial services to clients, ensuring commercial sustainability of partner organizations, and supporting policies and mechanisms to deliver services responsibly to clients.

The study considered only first loan cycle clients (in existence on MFI records for six months or less) as the universe wherefrom the sample was derived. This was a decision consciously made after MFIs expressed their need to learn about the poverty levels of client households at the point of entry into their system.

The report should be valuable for microfinance practitioners and funders interested in benchmarking data and typical client profiles.

Key Findings

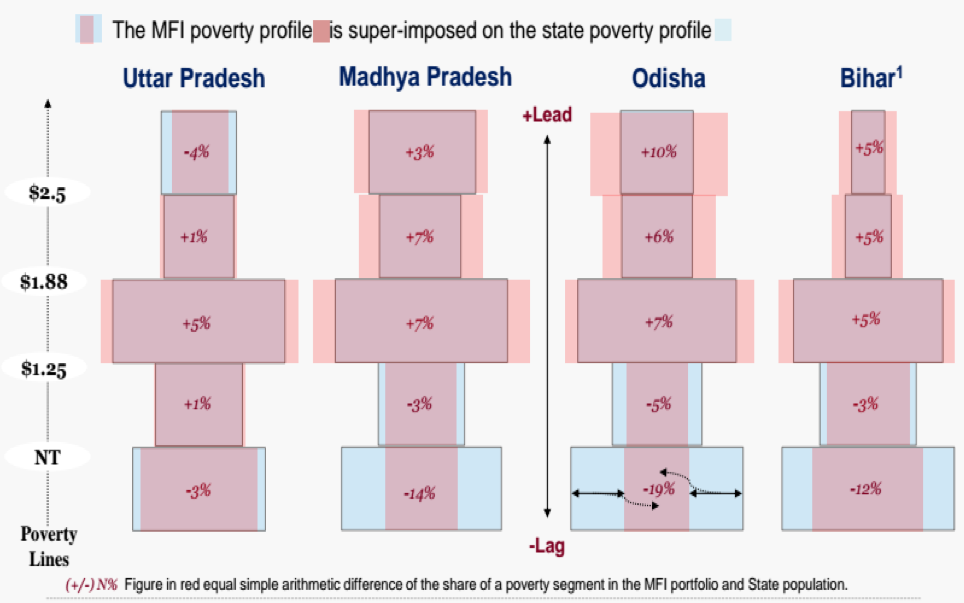

1. Except for a few regions, MFIs’ poverty outreach in the PSIG states is below the state-level poverty rates, especially in rural areas.

Ultra-poor and very-poor segments are not a natural outreach choice for microfinance institutions. MFIs admit that these segments do not show very steady cash flows or credit handling capabilities and may not be able to service debt sizes that are desired by microfinance operations. However, in the face of stiff competition from MFI peers, organizations are driven to seek out this second tier of potential clients.

The data above shows how the poverty concentration in the MFI portfolio compares with the regions they are located in. For all the regions, MFI poverty concentration exceeds state poverty for the segments between $1.25 and $1.88 poverty lines.

2. 50% of MFI clients classify in the poor and borderline-poor segments because of higher debt-servicing capacity of clients in these segments.

The “natural” selection of these poverty segments is because of the higher debt-servicing capacity of clients therein when compared to lower segments that may not have the financial prowess to service loan sizes that are favorable for the operational efficiencies of a MFI.. There is also a natural concentration of clients in the poor and borderline-poor segments in geographical areas with better access to infrastructure, making it easier for MFIs to reach out to them. It is more expensive to reach out to remote areas with poorer populations (very-poor and ultra-poor segments) given the higher operating costs involved. Such segments may be reached in due course once competition pushes MFIs to go into deeper territories.

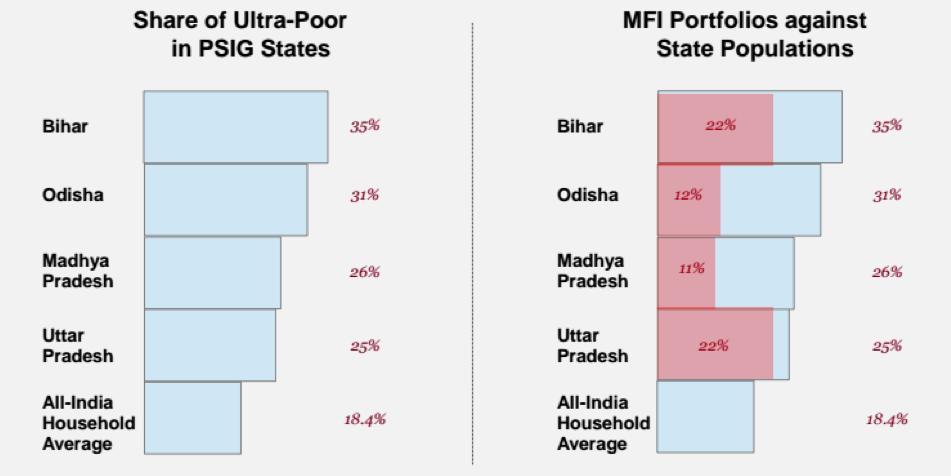

3. The ultra-poor segment is highly underserved by microfinance institutions and deserves to be addressed through a more enabling ecosystem – both for MFIs and clients.

The current products offered by MFIs (broadly at a sector level) have been tailored by keeping in mind the client needs, regulatory requirements and factors that influence MFI efficiencies to operate. With the products on offer and with the loan sizes being strived for, MFIs do not see the ultra poor segments as a natural fit. Most MFIs agree that working with the ultra poor segment will open up avenues to a larger market and also deeper poverty outreach. However, these have to be complemented by a more accommodating regulatory environment where MFIs can have the flexibility to cross subsidize product access based on a sound differentiation strategy. Clients in this segment definitely can be serviced through microfinance, the selection process has to be very stringent and requires an additional investment of time to minimize defaults.

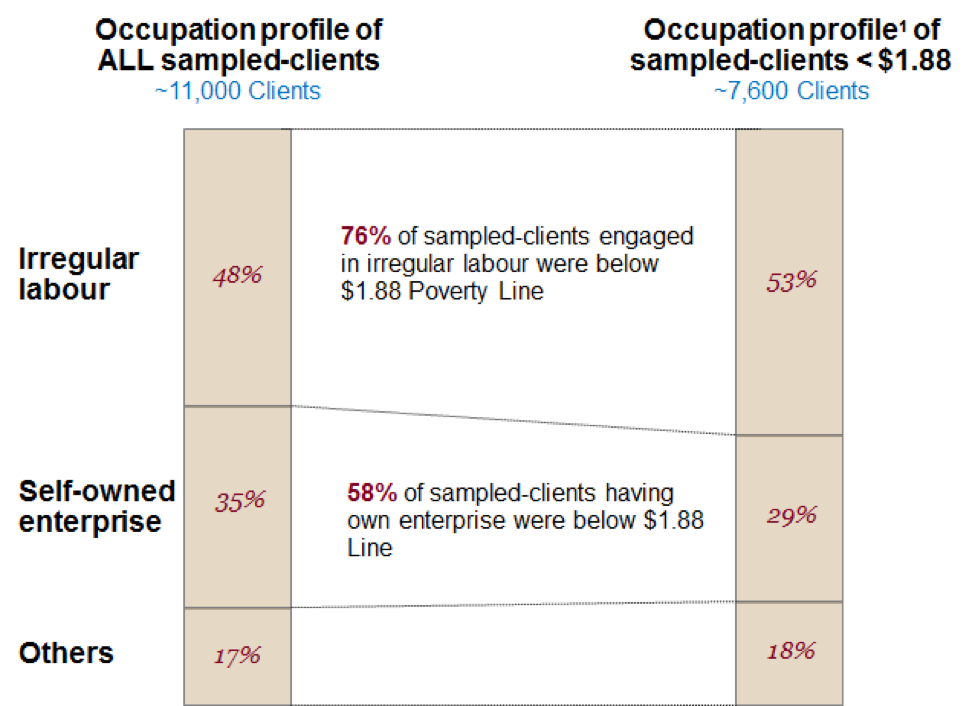

4. Occupation profile of microfinance clients:

Forty-eight percent of the clients recruited by the MFI earned their livelihood from “irregular labour”. For the purposes of this study, irregular labour is defined as inconsistent streams of income and mostly from wage labour. Further, wage labour was largely in farming activities since most of the study’s sample was derived from rural microfinance outreach. These are households that are not considered by formal banking institutions and typically MFIs are the only institutions that will ever serve them. When seen through a poverty lens, such client households are also the poorer when compared to their counterparts belonging to other livelihood groups. 76% of those engaged in irregular labour were below $1.88 poverty line at 2005 PPP. In contrast, of the 35% of total sampled households who are engaged in self-owned business enterprises, about 58% fall below $1.88 poverty line.

The Typical MFI Client Profile

Through this project, GFI has collected poverty data using PPI for almost 16,000 microfinance clients over a period of 3 years for 4 states in India - Bihar, Madhya Pradesh, Odisha, Uttar Pradesh and Karnataka. The insights gathered have afforded us the liberty to be able to draw some common characteristics of a typical microfinance client in the mentioned regions. Some of the following features stand out as common:

- The client is most likely to fall in the “Poor” or “Borderline Poor” category.

- The client household has irregular streams of income albeit involved in livelihoods with a running cash flow that can service microfinance loans.

- While the client is most likely to be a woman, most financial decisions rest with the male members of the household. In a majority of cases, loans are also being sought for enterprises run by male members of the household.

- The client household is most likely to also have overall low financial resilience with minimum to no access to formal credit and non-credit financial products.

Most of our understanding of the low income household segment in India and elsewhere is based on data that is collected and reported on an ad hoc basis with varying degrees of quality, authenticity and statistical relevance. The Poverty Outreach Report is a growing body of literature that is an effort by GFI to further the understanding of poverty segments that MFIs work with and offer recommendations that can be used to tailor products and services congruent with the needs of the segments served.

These and further details can be found in the full report.

Devahuti Choudhury is Principal Lead, Client Insights & Social Performance, Grameen Foundation India